Historical Background

At the beginning of the 19th century we experienced the first sugar crisis after sugar cane’s boom, which led to the bankruptcy of many smaller sugar estates and hence also the closure of the corresponding rum distilleries. Even though cane sugar can compete with beet sugar on the global market, the reality looks quite dire. Wages and working conditions for workers in many cane sugar producing countries are often miserable (see my article on Nicaraguan Rum) and quotas and tariffs surely do not help.

Historically, it all started when Napoleon introduced economic measures as an additional weapon in the Napoleonic Wars. His Continental System or Continental Blockade introduced a large-scale embargo against British trade in Novemeber 1806, following a naval blockade of the French coast by the British a few months earlier. This so-called ‘Berlin Decree’ banned the import of British goods into large parts of mainland Europe or at least introduced prohibitive tariffs, in our case on sugar from the colonies. Sugar beet boomed and by 1880 half of the world’s sugar has been derived from sugar beets. Today it is mainly the EU with their tariffs on cane sugar and subsidies on continental beet sugar that causes demand and prices for cane sugar to fall. As a result, there are only very few sugar estates left in the Caribbean, implying that molasses has become somewhat of a scarcity.

With cane sugar, the government-owned, debt-ridden Guyana Sugar Corporation (short: GuySoCo) has for a long time been one of the last entities to withstand the competition of sugar beet but now they look like they might be the next one to fall. For us, GuySoCo is especially interesting since they have been supplying most of the Anglophone Caribbean with molasses for the last several years, most notably Barbados, St. Lucia, Grenada, Antigua and St. Vincent. Run by the UK-based Bookers Group until it was nationalised in 1976, it was once the country’s largest source for foreign exchange with an average production of about 300,000 tons per year until the ’90s. Not only tariffs and falling prices but also labour strikes, manpower shortages and unseasonal weather are said to be reasons for the decline of the industry.

Falling Demand and Prices

A crucial turning point has been reached at the end of June 2017, when the EU indicated that they will put an end to the seven year spell of assistance which provided more than €1,39B to help Guyana recover form a 36% drop in sugar prices, which has been phased in in 2006 by a reform of the EU’s sugar regime (production quotas and minimum pricing) to allow for more beet sugar to flood the markets. Depending on the individual countries’ importance of the sector and impact of the reform, assistance has been granted to all of the countries that have been selling sugar to the EU to help them adjusting to the reform. In Guyana, another problem was that the money never went directly to GuySoCo but to the Treasury, who then decided how the funds should be used.

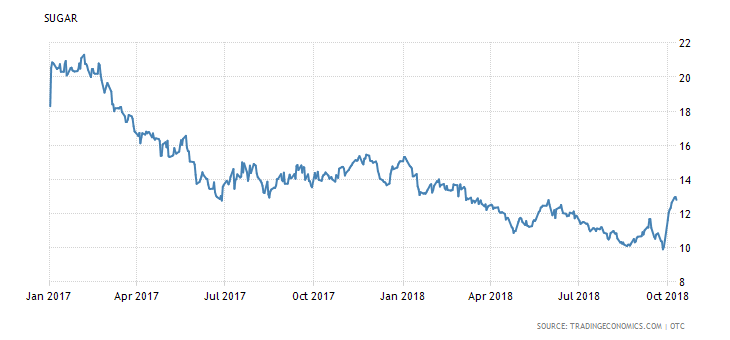

In May 2017, when prices were already falling (see figure above), the Guyanese government announced plans to scale back on sugar production with a target of 147,000 tonnes to satisfy local demand as well as that of the Caribbean Community (CARICOM), the US and the World Market. To that end, the Rose Hall and Enmore sugar factories were set to close by the end of the year, paired with a divestment of the Skeldon Sugar Factory. This would leave only Albion, Blairmont and Uitvlugt Estate. The reason for this was another 30% fall in global sugar prices, which meant that the cost of production was now almost three times of what GuySoCo has been selling for. Naturally, people started protesting but the government insisted that they cannot afford to finance and bail out a dying industry. 2,500 workers were planned to be retrenched by the end of the year and GAWU, the Guyana Agriculture and General Workers Union, estimated the loss of more than 15,000 jobs and the potential threat of poverty for between 50,000 to 100,000 people as a result of downsizings and closures.

In November 2017, the Special Purpose Unit (SPU), which has been established earlier in the year under the National Industrial and Commercial Investments Limited to manage the divestment process of GuySoCo, had yet to carry out works at the Rose Hall Estate to determine how to go about the factory. As a result, the closure of Rose Hall and Enmore was postponed from the end of 2017 to 2018 since there was no follow-up plan yet. In the meantime, a Private Sector Commissions has indicated interest in purchasing Enmore Estate and these proposals will be analysed by the SPU. Nevertheless, downsizing started already by New Years Eve. Hundreds of workers were laid off from the Rose Hall and Enmore Estates as they were closed. A little earlier, workers were already laid off from the La Bonne Intention and Wales Estates, which the government wanted to merge with Enmore and Uitvlugt, respectively. At the same time, two former sugar workers attached to the Uitvlugt-Wales and Rose Hall Estates reportedly committed suicide after not receiving their severance payments from GuySoCo. According to GAWU, “they seemingly could not bear the pressures of a jobless, misery-filled life…” as they were unable to even secure a part-time job. GAWU also noted that “while the two incidents are more extreme manifestations, the laying-off of thousands of sugar workers has been a serious psychological factor and is pushing some into a depressive, despondent and desperate state.” I think it is obvious how such a large structural change causes stress not only on the country’s economic future but also large parts of its population.

In July 2018, the government started the privatisation and divestment process of the Enmore Estate, with all machinery, CARICOM membership, and 6,900 hectares of land. A month later, PricewaterhouseCooper (PwC) also finished their valuation of the Skeldon sugar factory (1,750 hectares with an option for a 25 year lease on an additional 11,900 hectares of cultivated land) so that two facilities can now be assessed and acquired by interested investors. Skeldon, which recently added a co-generation plant, has historical been plagued by technical issues, likely impairing its price.

Molasses Shortages

On to 2018. Around Christmas 2017 we learned that Guyana’s sugar output was expected to fall by nearly a quarter from a year ago and the ~140,000 metric tonnes produced in 2017 were the lowest number in 27 years. Needless to say, the amount of molasses had to decrease as well. While, GuySoCo stated that they managed to meet its sugar production target for the second crop of 2018, reporting that “Albion, Blairmont and Uitvlugt have been performing satisfactorily thus far for the crop”, the respective weekly targets for the three production facilities combined have only been met 8 out of 21 weeks. This indicates a relatively high volatility in the weekly output. Anyways, other Caribbean countries have to look elsewhere for their molasses, which poses new questions on general availability, steady guaranteed supply, price and price volatility, transportation and general infrastructure as well as potential differences if the molasses comes from different cane varieties. Some countries (Barbados, St. Lucia, Grenada) have already gone back to planting sugar again, albeit at a very small-scale which is by no means sufficient to meet the demand for molasses.

What can be done?

Improvements in productivity already indicate that cane yields are expected to rise from the current 55 tonnes/ hectare to about 78.33 tonnes per hectare this year, which is a 41% increase. Moreover, GuySoCo is looking to produce plantation white sugar to counteract the changes in the EU’s sugar regime. Here, the strategy is to replace imports of refined sugar regionally. Moreover, Guyana is looking to file an application for a Common External Tariff on extra-regional refined sugar and the unit cost of production is expected to decrease to $0.25 per cubic pound of sugar with a number of additional identified cost saving initiatives which might lower the unit cost even further. A feasibility study financed by the EU is looking into the viability of cogeneration at Albion and Uitvlugt. Excess power could then be sold to the national grid. Moreover, prices started to increase again last months, but it has yet to be seen if this increase is persistent or not.

Another major problem which we have completely ignored so far is the large debt stock of GuySoCo, who have to pay huge amounts just servicing the debt every year. Hence it is clear how downsizing can only be an option when this goes hand in hand with huge increases in productivity for the remaining estates. But these are just some of the challenges that the industry is facing.